Nvidia Is Everywhere in Auto Tech Headlines. Here’s What That Actually Means

Nvidia has become the default name associated with high-performance computing for autonomous driving and advanced cockpit systems. From major automaker platform announcements to earnings call mentions, the company’s automotive momentum appears strong. Yet the gap between design wins, actual revenue recognition, and long-term market control deserves closer examination.

The Strength of Nvidia’s Position

Nvidia’s automotive business benefits from several genuine advantages. Its CUDA software ecosystem remains the standard for AI development in many autonomy teams. The DRIVE Orin and upcoming Thor platforms deliver high TOPS (trillions of operations per second) ratings that impress both engineers and investors. Several major automakers have publicly selected Nvidia silicon for next-generation ADAS and autonomous platforms.

This momentum reflects real demand for centralized compute capable of handling increasingly complex sensor fusion, planning, and increasingly generative AI features inside vehicles.

The Revenue Timing Reality

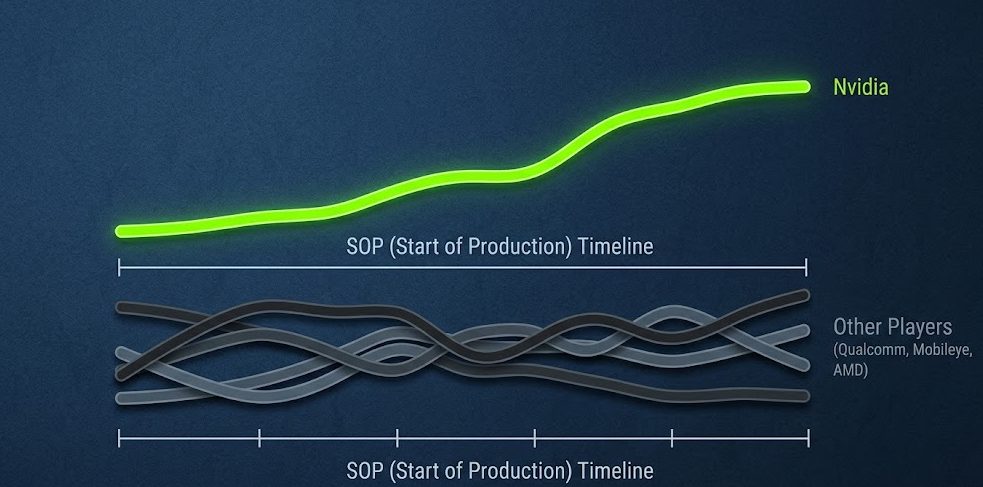

Design wins do not equal immediate revenue. Automotive product cycles are long — often 3 to 5 years from selection to start of production (SOP). Many of the high-profile “wins” announced today will only begin contributing meaningful revenue in the late 2020s or beyond.

This creates a situation where Nvidia’s automotive story looks extremely dominant in headlines while current revenue contribution remains relatively modest compared to its data center business. The hardware story and the margin story are not the same.

Key factors to watch include:

Actual production ramp timelines for announced platforms

Pricing pressure as automakers seek volume discounts at scale

The mix between high-end autonomy compute and more mainstream ADAS applications

Competition and Diversification Efforts

While Nvidia leads in performance-oriented AI compute, it is not without challengers. Qualcomm, Mobileye, AMD, and various in-house solutions from automakers are all competing for sockets inside future vehicles. Many automakers explicitly state goals of reducing dependency on any single semiconductor supplier after the chip shortage exposed supply chain vulnerabilities.

Some companies are pursuing multi-sourcing strategies or developing their own silicon to retain greater control over their technology stack. This pushback against single-vendor dominance is a rational response to both cost and resilience concerns.

Supply Chain and Business Implications

Nvidia’s success in automotive semiconductors strengthens its overall position but also highlights broader industry tensions. The demand for powerful automotive-grade chips increases pressure on foundry capacity, particularly at advanced process nodes. It also raises questions about who ultimately controls the software stack running on that silicon.

For Tier 1 suppliers and automakers, partnering with Nvidia provides access to leading AI capability but can limit flexibility in software differentiation. The balance between leveraging best-in-class components and maintaining architectural control remains a central strategic tension.

What This Means for the Industry

Nvidia’s prominence accelerates the trend toward software-defined vehicles by providing powerful centralized compute platforms. However, it also intensifies the battle over ecosystem ownership. Companies that rely heavily on Nvidia silicon must still build compelling software layers and user experiences on top of it.

Investors should separate the narrative of dominance from the slower reality of automotive revenue ramps. Real traction will be measured by consistent production volumes and contribution to Nvidia’s bottom line, not just platform selection announcements.

Risks and Uncertainties

The key uncertainty remains execution at volume. Automotive qualification standards are rigorous, and scaling advanced AI chips across millions of vehicles introduces thermal, power, and cost challenges that are still being fully validated in real-world conditions. Geopolitical factors and export restrictions could also affect global deployment strategies.

It is not yet clear whether Nvidia can convert its current design win momentum into sustained, high-margin automotive revenue without significant pricing concessions.

The Practical Question

Nvidia is clearly winning mindshare and many important design contests in automotive AI. That matters. But sustainable success in this industry depends on translating those wins into reliable, profitable, at-scale shipments while navigating automaker desires for diversification and cost control.

We will continue tracking Nvidia and the broader automotive semiconductor landscape with focus on production realities, not just PowerPoint leadership.